The survival of the American offshore wind industry depends on the delta between federal executive hostility and the entrenched economic momentum of state-level mandates. While the sector has recently celebrated the commencement of power delivery from projects like Vineyard Wind 1 and South Fork Wind, these milestones occur against a backdrop of fundamental political and fiscal instability. The "good news" of operational success is currently offset by the "bad news" of a looming executive pivot that threatens the three pillars of the industry: permitting certainty, federal fiscal incentives, and maritime logistics.

The Triad of Offshore Wind Risk

To quantify the stability of an offshore wind project, one must analyze the intersection of three distinct risk variables. The "Trump Effect" does not hit these variables equally; rather, it creates a tiered hierarchy of disruption. Also making headlines in this space: The Strait of Hormuz Chokehold and the Fragile Illusion of Asian Energy Security.

- Regulatory Velocity (Permitting and Bureau of Ocean Energy Management [BOEM] Oversight): The Executive Branch maintains nearly total control over the pace of environmental reviews and the issuance of Record of Decisions (RODs).

- Fiscal Architecture (Inflation Reduction Act [IRA] Tax Credits): While the repeal of legislation requires a Congressional majority, the Treasury Department holds significant power over the "interpretation" of domestic content requirements and credit eligibility.

- Logistical Constraints (The Jones Act and Port Infrastructure): Federal enforcement of maritime laws determines the cost and availability of Wind Turbine Installation Vessels (WTIVs).

The Permitting Bottleneck as a Policy Lever

The most immediate threat to the sector is the weaponization of administrative delay. The National Environmental Policy Act (NEPA) process, managed by BOEM, is the primary gatekeeper for project lifecycles. A hostile administration does not need to formally "ban" offshore wind; it merely needs to deprioritize the review process or increase the evidentiary burden for Environmental Impact Statements (EIS).

This creates a Capital Expenditure (CAPEX) Trap. Offshore wind projects are characterized by high upfront costs and long lead times. If a developer secures a Power Purchase Agreement (PPA) with a state but faces a three-year federal delay, the project's Internal Rate of Return (IRR) collapses due to: More information on this are detailed by Investopedia.

- Cost Escalation: The price of raw materials (steel, copper) and specialized labor continues to rise while the PPA price remains fixed.

- Cost of Debt: Extended timelines increase interest payments on construction loans before the first megawatt-hour is sold.

- Technological Obsolescence: Turbines specified in the initial design may be out of production by the time the project reaches "steel in the water," forcing expensive redesigns and re-permitting.

The Inflation Reduction Act and the Resilience of Fiscal Incentives

Much of the sector's current optimism relies on the Investment Tax Credit (ITC) and Production Tax Credit (PTC) frameworks established by the IRA. Critics of the industry argue that a Trump administration will dismantle these credits on day one. However, the mechanism of repeal is complex.

Tax credits are legislative products. Repealing them requires a "reconciliation" bill, which necessitates a GOP trifecta (House, Senate, and Presidency). Even with a trifecta, the geography of offshore wind investment creates a political friction point. Significant portions of the supply chain—specifically steel fabrication, cable manufacturing, and port revitalization—are located in states or districts that may be politically sensitive to the loss of manufacturing jobs.

The strategy for the industry under a hostile executive shifts from "growth" to "entrenchment." Developers are currently racing to "safe harbor" their projects. Under IRS rules, a project can lock in tax credit eligibility by:

- Starting physical work of a significant nature.

- Paying or incurring 5% or more of the total cost of the facility.

By front-loading these expenditures, developers attempt to make their projects "repeal-proof" under the principle of non-retroactivity in tax law. The risk remains that the Treasury could tighten the definition of "Domestic Content Bonus" credits. If the federal government mandates that 100% of sub-components must be U.S.-sourced—a standard current domestic supply chains cannot meet—the effective subsidy drops by 10%, rendering many projects unbankable.

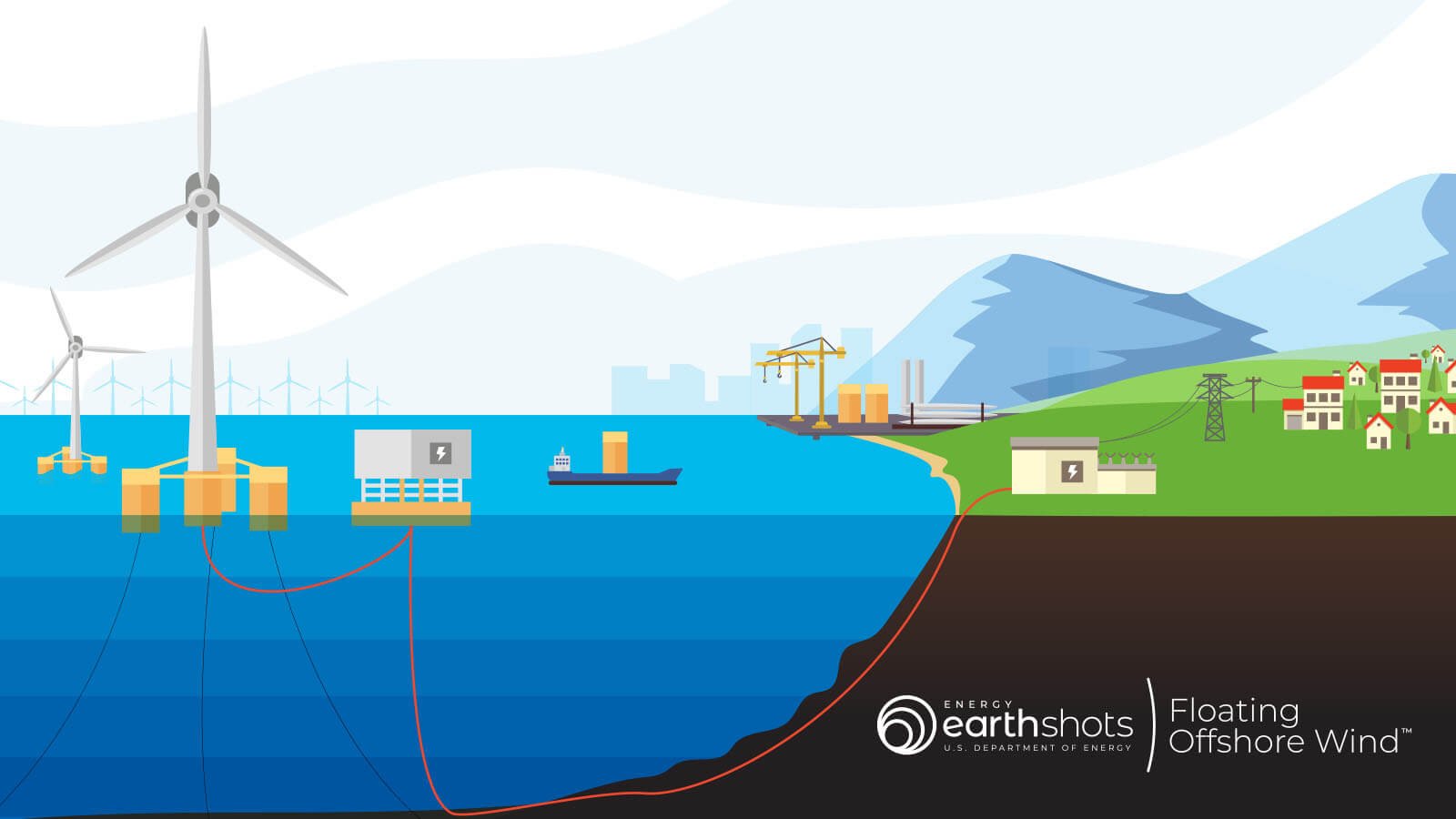

The Maritime Logistical Chokepoint

The Jones Act (Merchant Marine Act of 1920) requires that goods transported between U.S. ports be carried on ships that are U.S.-built, U.S.-flagged, and U.S.-manned. Since there is currently a global shortage of WTIVs, and only one U.S.-built WTIV (the Charybdis) is nearing completion, the industry relies on "feeder" solutions. Foreign-flagged vessels perform the installation while U.S.-flagged barges ferry components from the port to the site.

An administration focused on "America First" protectionism could issue executive orders or Customs and Border Protection (CBP) rulings that narrow the loopholes currently allowing foreign vessels to operate in U.S. waters. If the "stationary" installation vessel is redefined as "transporting" goods because it moves slightly during the construction process, the entire installation strategy for the Atlantic coast becomes illegal overnight.

This creates a binary outcome for project viability:

- Scenario A (Cooperation): Continued use of foreign heavy-lift vessels with U.S. feeder barges.

- Scenario B (Protectionism): Total halt of offshore installation until a domestic fleet is built, a process requiring a minimum of 4–7 years per vessel.

The Divergence of Federal vs. State Power

The primary counterweight to federal hostility is the statutory obligation of states like New York, New Jersey, and Massachusetts. These states have codified offshore wind targets into law (e.g., New York’s 9 GW by 2035).

This creates a Federalist Friction Point. While the federal government controls the seabed (OCS—Outer Continental Shelf), the states control the "offtake"—the actual purchase of the electricity. If a Trump administration halts new leases, states will likely respond by:

- Litigation: Suing the Department of the Interior for failure to execute its statutory duties under the Outer Continental Shelf Lands Act (OCSLA).

- Repowering Existing Leases: Focusing on increasing the density and turbine capacity of already-leased areas rather than seeking new acreage.

- Grid Hardening: Investing in the onshore transmission infrastructure required to accept offshore power, ensuring that once federal hurdles are cleared, the "last mile" is ready.

The Cost Function of Bad News

The "bad news" cited in industry circles often refers to the cancellation of major projects, such as Orsted’s Ocean Wind 1 and 2. These cancellations were not purely political; they were the result of a "perfect storm" of macroeconomic factors:

- $Inflation \approx +20-30%$ on specialized equipment.

- $Interest Rates \approx 500$ basis point increase from project inception.

- $Supply Chain \approx 24-36$ month delays for high-voltage subsea cables.

When political uncertainty is added to this equation, the "risk premium" demanded by equity partners increases. A project that was viable at a 7% Weighted Average Cost of Capital (WACC) becomes a stranded asset at 10%.

Strategic Positioning for the 2025–2029 Cycle

To navigate the next four years, the offshore wind industry must move away from "climate-centric" messaging and toward "energy security and industrial base" messaging. The logic of "good news" in this sector will no longer be measured by environmental metrics, but by the following operational milestones:

1. Hardening the Supply Chain

Developers must prioritize "Tier 1" suppliers with domestic footprints. This reduces exposure to both Jones Act volatility and potential tariffs on imported steel or Chinese-manufactured sub-components. The goal is to reach a "Critical Mass of Employment" in swing districts, making the industry politically expensive to dismantle.

2. PPA Flexibility and Inflation Indexing

Future contracts between developers and state utilities must include "inflation adjustment" clauses. The rigid PPAs of the 2018–2021 era are the primary reason for current project cancellations. Moving to a dynamic pricing model protects the developer from the fiscal volatility of a shifting federal landscape.

3. Exploiting the "Blue Economy" Narrative

The offshore wind industry must align with Department of Defense (DoD) and maritime interests. By framing offshore wind substations as dual-use infrastructure for maritime surveillance or coastal defense, the industry can tap into "Deep State" institutional support that persists regardless of the individual in the Oval Office.

The "bad news" of the Trump era is not the end of the industry, but the end of its "subsidized adolescence." The coming years will force a brutal consolidation where only the most capitalized and politically integrated projects survive. The transition from speculative growth to hardened industrial execution is the only pathway to long-term viability. Success will be defined not by the number of leases signed, but by the number of foundations successfully piled into the seabed before the next regulatory shift.

The immediate strategic play is clear: accelerate all "physical commencement" of work before January 2025 to secure tax credit safe harbors, while simultaneously pivoting all lobbying efforts toward the economic defense of domestic manufacturing jobs. This is no longer a green energy play; it is a heavy industry survival play.